How Crypto Is Shaping the Digital Revolution

I have previously categorized ’crypto’ — a catch-all for blockchain- and Web3-related innovation — as part of the Digital Revolution that started around the late 1960s to early 1970s with the invention of packet switched networks, microprocessors, and other digital technologies that enabled the proliferation of personal computers and the Internet. I would like to expand on that by:

- Providing a brief theoretical outline of the two main stages of technological revolutions;

- Comparing the organizational and institutional shifts of the previous revolution (centered around oil, automobiles, and mass production) with those of the current one (centered around digital information and communications technology) as imagined during the dot-com era (late 1990s, early 2000s); and

- Discussing how ’crypto’ as a techno-populist reform movement and innovation cluster is shaping global institutions and governance as the Digital Revolution matures.

Throughout the text, I will be using ’ICT’ as a shorthand for digital information and communications technology, and ’ICT Revolution’ as a shorthand for the Digital Revolution. From here on, quotation marks around the word ’crypto’ will be omitted, while still referring not just to cryptography, but to all blockchain- and Web3-related innovation. Readers familiar with Carlota Perez’s theory of techno-economic paradigm shifts may skip the first section.

From Installation to Deployment

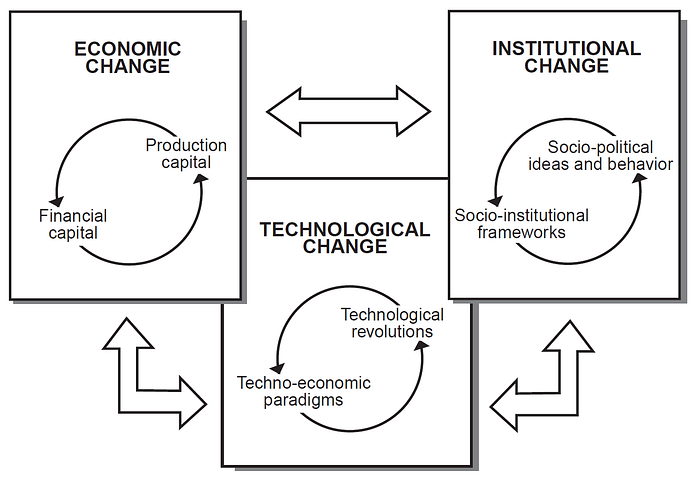

A popular model for theorizing economic development is that of wave-like cycles. There are many variants of this approach, each focusing on a different set of change drivers, including demographic, credit/debt, trade, and political cycles. In innovation economics, with roots in the work of Joseph Schumpeter, the main emphasis is put on entrepreneurship and innovation.

Within the neo-Schumpeterian tradition, Carlota Perez is known for her contributions to the theory of technological revolutions and techno-economic paradigm shifts that divides modern economic history into five surges of development. Each surge has been driven by a different set of revolutionary technologies, initially adopted in a few leading countries, and then gradually spreading to other parts of the world. For example, the fourth paradigm that started to take shape in the United States in the early decades of the 20th century was centered around oil, automobiles, and modern methods of mass production that enabled suburbanization and consumerist lifestyles. Later in the century, and still ongoing, the fifth paradigm has been driven by innovations in ICT, including digital electronic computers and the Internet — the core technologies of the Information Age.

In Perez’s model, each surge is triggered by a ’big bang’ event (usually a key technological advancement, such as Stephenson’s Rocket steam locomotive, Ford’s Model T automobile, or Intel’s 4004 microprocessor), spans approximately 50–60 years, and is divided into four distinct phases. The first two phases, called Irruption and Frenzy, constitute the installation stage of the revolution. During this period (1970s to early 2000s in the case of the ICT Revolution), the new paradigm and its key industries are still forming (which increases the role of speculative financial capital), while individualism combined with lagging regulation contribute to a highly uneven distribution of gains from innovation. Installation periods culminate in a crisis — a mid-stage turning point of the revolution. The latter two phases, called Synergy and Maturity, constitute the deployment stage. According to the model, this is when production capital tends to dominate (i.e. non-financial firms engaged in the production of real goods and services), leading industries consolidate, and ideally, a more equitable distribution of economic gains is achieved through progressive institutional reform and a revised social contract. [1]

A key proposition of the theory of techno-economic paradigm shifts is that, while its prerequisites are put in place during installation, the broader social and institutional transformation enabled by the new paradigm can only be realized in deployment. This is because the full potential of the revolution reveals itself over time through continuous learning, iteration, and especially synergies between different clusters of innovation as they mature. Also, compared to the techno-economic sphere, which is more easily stirred by entrepreneurial initiative and competitive pressures, the socio-institutional sphere tends to be more resistant to change and requires extreme political and cultural pressures — a crisis — before it can dispense with existing structures and habits. But eventually, the technologies and organizational principles of the new paradigm become normalized and deeply enough embedded throughout society that even the most conservative institutions are forced to adapt. As the revolution propagates, the economic and social logic that characterized the previous revolution (or even the installation stage of the current one) is increasingly viewed as anachronistic. The techno-economic paradigm established by the revolution becomes a ’new normal’, serving as a starting point — as well as a source of inertia and resistance — for the next wave of innovations with potential to revolutionize the whole economy. And so the cycle repeats. [2]

The outline above is somewhat mechanical. In reality, each revolution has many unique characteristics that make such sweeping generalizations problematic. But, as a starting point for connecting crypto with the ICT Revolution, the core distinction between installation and deployment is sufficient. Stated simply, crypto can be viewed as a typical early deployment stage reaction to the ICT Revolution, enabling more digitally-native institutions, lifestyles, and forms of governance. [3] But before exploring this idea in more detail, it is important to recognize how crypto builds on earlier forms of digital transformation, and highlight some of the context in which it has emerged.

Deployment of Mass Production vs. ICT Revolution

There are two primary forces that shape the deployment stage. First, the continued iteration and mass adoption of the core innovations of the revolution that establish the new paradigm in everything from production methods and business organization to consumer lifestyles and social institutions. And second, public policies in reaction to the challenges and opportunities created by the revolution. Although separate, these two forces are in constant interaction: the invention and adoption of new technologies affects policymaking, which in return shapes the evolution of technology, and especially the social distribution of the costs and benefits of innovation.

During the first two thirds of the 20th century, led by the United States, developed economies around the world adopted the technologies and organizational principles of the mass production paradigm. Most importantly, this included automobiles and other machines with internal combustion engines, powered by affordable oil-based fuels. The assembly-line version of Taylorism — ’scientific management’ — was applied across the industrial spectrum to coordinate the mass production of electrical home appliances and numerous other standardized consumer products, many of which were increasingly made from synthetic (petrochemical) materials. Private cars allowed living further from metropolitan centers, which drove the expansion of highways and road networks. The suburban consumerist lifestyle became not just a popular ideal but increasingly feasible for many, often with the help of government-backed housing loans and the optionality of paying for big-ticket items in installments. [4]

During the second half of the Mass Production Revolution, organizational practices pioneered by private companies were increasingly replicated in the public sector, which grew into a complex ’divisional’ structure similar to the large hierarchical corporations that dominated the economy. The same can be said about international organizations such as the United Nations, the International Monetary Fund, and the World Bank. In addition to supporting the housing market, governments also emerged as a major source of demand through public procurement of physical infrastructure (partly driven by the need for post-war reconstruction), as well as military spending motivated by the Cold War. The relatively strong position of labor unions made it difficult for productivity increases to decouple from wages, while welfare and unemployment insurance schemes helped soften the blows from economic downturns. All in all, although far from perfect, the positive synergies between technological advancement and public policy resulted in several decades of stable and inclusive growth in most Western countries — a typical example of what Perez refers to as the ’golden age’ of deployment. [5]

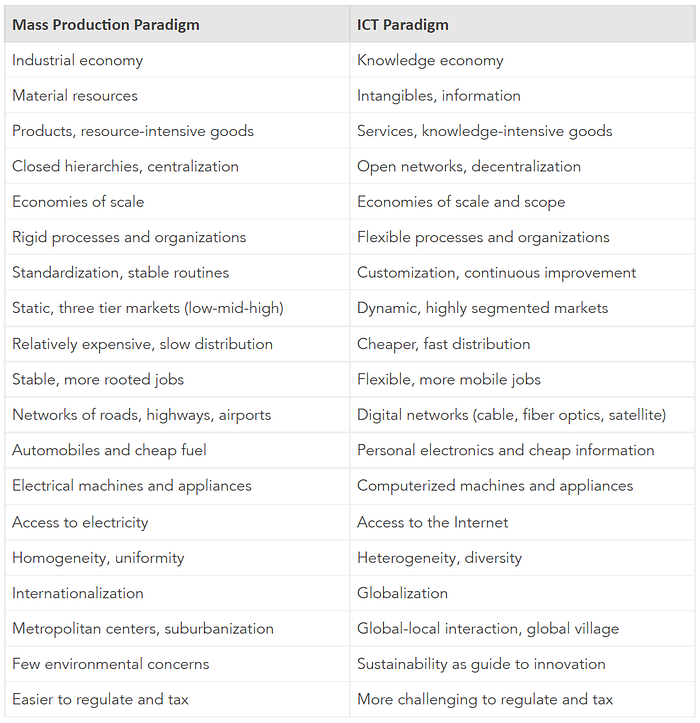

By the final third of the 20th century, and especially the dot-com boom of the 1990s, it was widely acknowledged that advanced economies were entering a new stage in their development. Terms such as post-Fordism, post-industrial society, knowledge economy, and information society were popularized as labels for this shift towards a more (information) technology-intensive and globally integrated economic order. [6] The table below highlights some key differences between the declining (left column) and the newly emerging paradigm (right column), as envisioned in the early 2000s.

Remember, according to Perez’s model, the dot-com crash represented only the approximate midpoint of the ICT Revolution — the whole deployment stage was still ahead. In the early 2000s, Perez wrote:

“Financial capital has already done its job of leading the intensive spread of the new paradigm and the installation and testing of the new infrastructure. Sufficient portions of the business community and of consumers have assimilated the new common sense to be able to continue the transformation process. Now is the turn of production capital to take the leadership, expanding production and widening demand, with financial capital in a supporting role. […] There is also ample scope for redirecting business imagination and technological innovation towards the deeper transformation of world society, through developing truly knowledge intensive ways of producing and living.“ [8]

The effect of the ICT Revolution on world society over the past twenty years has indeed been transformational. While there are still major social and geographic disparities in the adoption of ICT (the so-called digital divide), the ability to personally access and exchange information cheaply and near-instantly across the globe has undoubtedly improved the lives of billions of people. The overall impact is comparable to how the ability to mass produce and internationally distribute affordable consumer goods enhanced material standards of living in the 20th century as networks of production centers, shipping terminals, airports, and highways were built out at scale. This time around, the key enabling infrastructure are digital networks that connect data centers and personal computing devices, further accelerating the speed at which goods, people, and information can move, and thereby also the rate at which current best practices in all fields of life can disseminate on a global scale.

It is important to recognize that the diffusion of a new techno-economic paradigm is not an orderly process. Scattered throughout the multi-decadal S-curve of each technological revolution, there are numerous S-curves of individual revolutionary technologies, many of which become possible only after earlier ones have matured, and can easily re-disrupt industries still in the process of integrating a previous set of innovations. Recent examples include social media, automation of e-commerce, smartphones, cloud computing, internet of things (IoT), deep learning, advanced robotics, and blockchain technology. While the radical innovations of the installation stage (e.g. personal computers and the Internet) may appear more fundamentally disruptive, the deployment stage is equally transformative. In short, a new techno-economic paradigm never emerges fully formed but continues to evolve and unlock new synergies, in an increasingly iterative manner, throughout the revolution.

Perez’s concept of a ’new common sense’ that drives and enables the deployment stage is perfectly encapsulated in Marc Andreessen’s famous phrase “Software is eating the world.“ [9] But being eaten is not a welcome prospect. Each successive revolution presents an existential threat to the established ways of doing things, producing a mismatch between the new economic and technological reality on the one hand, and the established institutional, social, and regulatory frameworks on the other. [10] Throughout the past couple of decades, this mismatch has been an important source of social and political tension — a typical turning point pattern observed in all technological revolutions. Even today, when ICT is no longer a novelty, it is still associated with major challenges for both national and global governance as societies around the world cope with disruptions in economic structure, the division of labor, and the distribution of wealth and power triggered by innovation.

Despite historical patterns, however, the social world remains fundamentally uncertain, and one should be careful not to become overly deterministic when describing the dynamics of technological change. For example, while the latter half of each technological revolution has generally been a time of more inclusive economic development, it is by no means guaranteed. As Perez puts it, each deployment stage has the potential to be a ‘golden age’ for the majority of the population (at least in the core countries), but only if it is given an appropriate direction through a rebalancing of interests between financial and production capital, workers, and the state. [2] This is where post-crisis environments present a unique opportunity to mobilize different stakeholders and the necessary resources around a path forward that takes full advantage of the latest technological capabilities while also addressing the institutional and distributional shortcomings of the more turbulent installation stage. However, the vision for the right path is never universally shared and is therefore subject to political debate and struggle.

Two recent developments in particular are proof that the typical makings of deployment — at least as envisioned by Perez — are not preordained. First, despite much public discussion on fundamental policy reforms around issues such as income and wealth inequality, job insecurity, and environmental degradation, the actual steps taken have been rather incremental. And second, the size and importance of the financial sector has not decreased; to the contrary, the global economy appears increasingly financialized. [11] In the past, the regulatory response to events such as the Global Financial Crisis (GFC) of 2007–09 was often more radically progressive, serving as the backbone of a qualitatively different policy regime compared to the pre-crisis period. In contrast, the response to the GFC set the world up for roughly more of the same. While it is still too early to assess the full social and economic impact of the second half of the ICT Revolution, it has certainly been more mixed than what the idealized version of Perez’s model suggests. [12]

The concept of deployment can be applied prescriptively as a policy-driven ‘golden age’ (defined through historical comparison), or descriptively as whatever is observed in contemporary society (regardless of how well it maps to historical precedent). The analysis below leans more towards the latter and avoids the discussion of prescriptive policy in addressing the downsides of technological disruption. The continued iterations and mass adoption of ICT over the past two decades are historical facts, regardless of whether the related social and economic outcomes meet one’s personal expectations or the politically agreed upon objectives in any particular society. The observation that ICT has transformed organizational practices in most sectors of the economy is now trivially obvious. But the process is still ongoing, and it is only recently that signs of truly ICT-native forms of organization have started to emerge. The next and final section explores how crypto is shaping the evolution of digital institutions and governance as the ICT Revolution matures.

Crypto and the ICT Revolution

Attempts at defining the core innovation and societal significance of crypto are often compared to the parable of blind men and an elephant — a situation in which a complex phenomenon is described from different but limited perspectives. The most common interpretations can be divided into two categories, sometimes referred to as ’money crypto’ and ’tech crypto’. The first focuses on the impact of crypto on money and finance, and especially its potential to undermine the role that national governments and other centralized institutions have traditionally played in these areas. The second interpretation is even more ambitious, focusing on the impact of crypto on any digital system or service that might benefit from higher transaction execution guarantees, or a more decentralized, secure, and user-centric model for administering information.

The view presented here incorporates both ’money crypto’ and ’tech crypto’, and references Perez’s two-stage model of techno-economic paradigm shifts to explain how crypto fits into the ICT Revolution. More concretely, by considering crypto as a techno-populist reform movement, as financial innovation, as process and institutional innovation, and finally, as part of a general trend towards networked automation, it frames blockchain-related innovation as typical of the deployment stage. Given that the ICT Revolution is still ongoing, this interpretation is by definition a conjecture, the accuracy of which can only be assessed in retrospect once ICT has given way to whatever the next technological revolution will be based on.

Crypto as techno-populism

Historically, the mid-stage turning point of each technological revolution has been a time of heightened controversy and antagonism between different visions of the appropriate path forward. Financial and economic crises often lead to the questioning of the existing institutional order, widening the Overton window for fundamental reform. Turning points thus provide favorable conditions for political and social movements to tap into popular dissatisfaction with the status quo.

To understand the first way in which crypto can be related to the sequential structure of Perez’s model, it is important to recognize the reactive and ideological drivers behind crypto. These drivers are not uniform and are widely accompanied by more prosaic motivations, chief among them pure financial greed. But the discourse on crypto’s core value proposition is filled with direct criticisms of the dominant players in finance and digital technology who have benefited greatly — and according to many, disproportionately — from the ICT Revolution, not only during the pre-GFC economic expansion, but also through the post-crisis policy response. It is therefore rational to describe crypto as a techno-populist reform movement driven partly by dissatisfaction with the existing financial system and the excessive concentration of data, profits, and power within the digital economy — arguably one of the most important legacies of the ICT Revolution to date.

In addition to leaning critical towards incumbent institutions (many of which are working hard to secure their share of the potential new pie created by blockchain-related technologies), crypto is also an expression of the belief that innovation and incentive alignment, if appropriately channeled, can provide the foundation for a more technologically advanced, prosperous, and inclusive economy. However, it would be wrong to conclude that crypto is therefore a thoroughly progressive movement. Instead, as is often the case with groups that share an enemy but are too young and diverse to have a unified vision of what an alternative system would look like in practice, crypto accommodates the full range of political ideologies. Over time, certain ideological factions may emerge as dominant while others become marginalized, affecting the ways in which the existing political system engages with crypto as a whole, and more importantly, with individual blockchain networks and their respective communities that may differ considerably in their political positioning and governance.

The emergence of crypto as a social and political movement required the maturation of enabling technologies, the rise of Big Tech, and the favorable conditions of a turning point triggered by a financial crisis. In the end, similar to other post-crisis reform movements, its primary challenge is to erect a sustainable alternative to the structures it seeks to replace — or at least meaningfully improve upon — without being co-opted by the powers that be, or reproducing other known institutional failures. But while some sections of crypto have their long-term sights on the digital and creative economy more broadly, thus far, it’s in the fields of money and finance where the transformative potential of crypto has attracted most interest and activity.

Crypto as financial innovation

From a strictly financial perspective, crypto appears — at least on the surface — to contradict Perez’s idealized version of deployment in which highly speculative and self-referential forms of finance diminish in comparison to those that are more tightly coupled with the production of real goods and non-financial services. However, there are at least two reasons why using this frame is too limited to analyze crypto and the context in which it has emerged. The first focuses on the relationship between financial and production capital, and more generally the adoption and real-economic effects of ICT since the early 2000s, while the second frames crypto-financial innovation as entirely consistent with — and indeed, explicitly anticipated by — Perez’s theory.

First, it is certainly true that the aftermath of both the dot-com stock market crash and the GFC ended up doing little to reduce financialization. In many leading countries, the size of the financial sector and the importance of financial instruments in facilitating economic processes has not decreased. In relative terms, financial capital has not given way to production capital (which in many Western countries has been declining anyway due to deindustrialization), and the line between the two has generally become more blurred. [13] This has been enabled partly by the impact of loose monetary policy on the financial sector, partly by the weakness of post-crisis reforms in discouraging financialization, and partly by digital technologies (including crypto) that have greatly improved access to financial knowledge, tools, and markets, both for retail and institutional participants. In addition, the ICT Revolution coincided with the global rise of technology-focused venture capital and crowdfunding over the Internet that have subsidized continued experimentation and growth in both traditional fintech and crypto, especially after the GFC. [14]

However, the relative size of the financial industry should be viewed in a broader context of ICT’s impact on society. In absolute terms, the role of production capital in the mass rollout of digital infrastructure, products, and non-financial services over the past two decades — a core feature of the deployment stage — has been nothing short of impressive. In addition to Big Tech, which now includes some of the largest companies in the world, there’s a long tail of other well-established firms that have delivered digital information and services to the fingertips of tens of millions of organizations and billions of individuals — certainly in the leading economies, but increasingly also in the less developed regions of the world. [15] In short, the digital and the intangible in everyday life, work, and consumption have become important aspects of the real economy, even if not always accounted for by traditional economic measures.

Second, although the use cases for crypto extend to the administration of information more broadly, it is in the fields of money (cryptocurrencies) and financial services (decentralized finance) [16] that blockchain and related technologies have been most impactfully applied to date, which illustrates the changing nature of financial innovation at different stages of a technological revolution. According to Perez [17], the installation stage tends to coincide with more favorable conditions for real financial innovation (i.e. fundamentally new products), and it is widely agreed that the period from the early 1970s to the GFC (the installation stage of the ICT Revolution) was indeed financially innovative. [18] However, it would be incorrect to conclude that crypto as post-crisis financial innovation is incompatible with Perez’s model. Here’s how Perez describes the typical nature of financial innovation and reform after the mid-stage turning point:

“Though they are more likely to originate in governments or world institutions, some of the new rules in the area of finance are self-imposed, precisely to avoid the need for government supervision. They usually involve a new framework for banking and monetary practices. Next to them rules of the game are established to condition business [and labor relations], as well as regulatory innovations on the international level. But each set of regulations is unique because it needs to match the specific characteristics of the paradigm it is accommodating. […] Accountancy and disclosure legislation is usually enacted to avoid the specific abuses revealed during the previous Frenzy.“ [19]

“To help bring about this new prosperity [of deployment], innovations geared to smooth operation in the context of the new paradigm will also be necessary in money, banking and financial practices. As with all innovations, the date of introduction is less significant than the time of intense diffusion. Already the… installation period of each great surge brings forth multiple innovations in the field of finance. Some are temporary or doubtfully legitimate and are destined to disappear or become… marginal (for the time being). Others, especially those connected with accommodating the investment, production, trade and consumption processes of the new technologies will probably generalize and expand. The propagation of the paradigm to further and further branches of the economy in the deployment period is likely to require those very instruments, together with others tailored to the emerging business practices [for example technology-focused venture capital and crowdfunding over the Internet, both of which have been essential to the growth of the digital economy, including crypto — M.L.]. These might include innovations in types of money, banking services and forms of credit or finance, which create the facilitating conditions for the full adoption of the new paradigm across the whole… economy in each country and in the world. They would be closely coupled with those measures of public policy (national and international) that establish the rules of the game and the institutional framework for banking and finance. […] It is clear that the burgeoning knowledge economy [created by the ICT Revolution] will require a very wide range of new instruments and even the overturning of some ’eternal truths’ about the tangible nature of assets [which is exactly the challenge posed by crypto — M.L.].“ [20]

The passages above lend themselves to two diverging interpretations when it comes to the empirical record of the past twenty years of applying ICT to finance, which has enabled both conventional fintech and crypto. On the one hand, crypto is the exact opposite of government- or policy-led financial reform, nor can it be considered an attempt at self-regulation by the incumbent financial institutions. Although increasingly popular in certain sections of society in both developed and developing economies, crypto-financial services are still very far from mainstream adoption, and their impact on business and work outside of a handful of niche markets is still to be determined. So one possible conclusion is that, even though digital technologies as a whole have been instrumental to the modernization and globalization of finance over the past couple of decades (at least partially matching the specific characteristics of the ICT paradigm), it has not yet led to a deeper reform of the financial system, neither through government or self-regulation, and certainly not through crypto.

On the other hand, crypto is often framed exactly as a “new framework for banking and monetary practices“ that taps into the unique technological and organizational capabilities created by the ICT Revolution, arguably more so than conventional fintech which, although digital, is still rooted in traditional business methods. Financial revolutions are usually triggered by two types of advancements: legal-transactional (financial contracts, or terms of engagement more broadly) and technological-informational (communications infrastructure). Crypto involves both: cryptographic protocols (including smart contracts) in the first case, and blockchain networks combined with advanced ICT infrastructure in the second. The core values and organizational principles of crypto are free and open source software (FOSS) [21], decentralization, censorship-resistance, permissionless access (via off-the-shelf devices), and a level of transparency that is sufficient for anyone with some basic technical capacity to be able to audit and verify information. Thus, an alternative conclusion to the one above would be that crypto enables the most ICT-native form of financial services that exists today and, as such, creates the potential for a fundamental alignment of the global financial system with the ICT paradigm.

It is true that crypto-financial services are still marginal by the standards of conventional finance. However, crypto is both digital and global at birth, and therefore challenging to regulate and constrain through traditional, nationally embedded frameworks. This provides crypto with considerable potential for organic growth, contingent on addressing some key obstacles to its mainstream adoption. Most importantly, these include scaling with minimal tradeoffs in terms of security, decentralization, and privacy; improving the unfamiliar user experience; reducing the still relatively high risk of financial loss due to fraud, hacks, or software bugs [22] (as opposed to pure financial or market risk, which obeys a logic similar to other sectors of the economy); and ensuring a necessary level of systemic stability [23]. In all four cases, as well as other shortcomings of crypto vis-à-vis traditional finance, the role of visionary discourse in continuously attracting entrepreneurial and technical talent, financial investment, and a steady inflow of new users, will remain critical to crypto’s long-term success. [24]

The fact that crypto is challenging to regulate through traditional measures does not mean that regulation won’t be central in determining its future. The following aspects of the dynamic between regulation and crypto are particularly important:

- Traditional regulatory action, which may both encourage and hamper crypto’s growth, and will likely continue to be targeted at centralized service providers such as fiat on-ramps, custodians, and exchanges, but also at companies closely involved in the core software development or marketing of specific crypto-financial protocols and services.

- Crypto as a forcing function that drives traditional financial and regulatory institutions to explore new technologies and organizational models, the best examples of which are the growing interest in central bank digital currencies (CBDCs) [25] and attempts to integrate crypto with traditional finance and real-economic processes.

- Crypto as an expression of ‘code is law’ — the idea that software can replace traditional legal codes, not only by providing the basis for law as legal text, but increasingly also in terms of administration and enforcement by determining the types of actions possible in a world saturated by digital technologies. Behind the apparently anti-regulatory stance of crypto, there is also a vision of a world highly regulated by software protocols — the digital equivalents of bureaucratic rules of procedure. [26]

A common criticism of crypto is that it delivers few truly innovative financial products and merely recreates, on blockchains, everything that already exists. To a large degree, that is true. However, apart from all the novel software involved, the core innovation of crypto is not product but process and institutional innovation related to FOSS development, decentralization, open access, composability, programmability, automation, and distributed governance. All these concepts can be viewed as paradigmatic to the ICT Revolution that help enable “truly knowledge intensive ways of producing and living,“ as anticipated by Perez twenty years ago. Thus, to fully understand the societal significance of crypto, it is important to recognize its potential impact beyond just money and finance, on digital organizations and Internet-native social and economic coordination more broadly.

Crypto as process and institutional innovation

The diffusion of a technological revolution is a multi-decadal process, involving numerous revolutionary technologies around which clusters of innovative activity expand and mature at different points in time. There are core, general-purpose technologies that are iteratively improved upon throughout the revolution (digital computers in the case of the ICT Revolution, for example), but also a whole range of disruptive technologies that emerge only after earlier ones have sufficiently matured (public Internet, cloud computing, and smartphones, for example). Meanwhile, as the revolution progresses, many technologies become commodified, unit costs come down considerably, and growing parts of the population not only learn to rely on the new capabilities enabled by technological innovation, but begin perceiving it as the only ’normal’ way to live, work, and organize in contemporary society.

In the case of the ICT Revolution, the ’normal’ is digital. [27] However, the exact nature of the digital has changed considerably over time in a complex, co-evolutionary dynamic between technology, consumer behavior, and the activities of investors, private companies, and public institutions. This evolution is still ongoing with crypto among the key recent developments, giving birth to a whole new cluster of experimentation that revolves around digital information tracked on distributed ledgers. Although initially focused on money in the form of decentralized cryptocurrencies, this experimentation has quickly expanded into reimagining how various other types of digital infrastructure and services are finance, built, deployed, governed, and consumed.

Crypto as process innovation is focused primarily on the administration of information (including format, storage, transactions) and governance (including software and organizational development). [28] In its most ambitious visions of the future, by leveraging the power of technology to make these processes more transparent, decentralized, and autonomous, crypto aspires to complement and, in some cases, fundamentally disrupt the existing institutions of money, law, and digital platform. Crypto can therefore be framed as part of — to use Perez’s terminology [29] — the ongoing deployment stage of the ICT Revolution, which includes the emergence of ICT-native forms of organization and a broader alignment of both existing and emerging institutions with the ICT paradigm. More specifically:

- The open and permissionless nature of public blockchains makes them comparable to public infrastructure or utilities. However, whereas most public infrastructure is fixed in a specific location and is often either directly or indirectly controlled by democratically accountable institutions (i.e. government), crypto as digital infrastructure is inherently global (the closest existing analogue being the Internet) and controlled — decentrally — by the private sector. That does not mean that individual networks or services can’t or won’t have a relatively larger footprint in specific geographies, or that democratic checks and balances or accountability are fundamentally incompatible with crypto. But, in principle, crypto has a global reach from the outset (contingent only on access to the Internet) and is explicitly designed to be resistant to centralized control, either by government or any other group or organization. [30]

- Similar to the impact of crypto on finance, its entrance into other institutional fields presents a direct competitive challenge to, and is likely to trigger reactive changes within, incumbent institutions. From the point of view of the incumbents, this is best encapsulated in asking the question: “What is our crypto strategy?“

- Crypto creates a very open and dynamic environment for running digital governance experiments, not only in terms of governing blockchain-based networks and protocols (which can be thought of as digital institutions), but also in terms of using these networks and protocols as tools of governance in other contexts (i.e. as contributing to the digital transformation of traditional institutions). [31]

- Crypto enables new forms of online coordination and community-building, including decentralized autonomous organizations (DAOs), that were not possible prior to the invention of public blockchain networks. These communities and organizations are unique to the economic system that is forming around assets, contracts, and relationships tracked via blockchains. [32] Over time, this emerging crypto-economy may increasingly challenge — or become integrated with — more traditionally organized parts of the digital economy.

Alongside blockchains and FOSS protocols, DAOs are essential to crypto as institutional innovation. DAOs can be defined as organizations that combine automation (via distributed computer networks and smart contracts) [33] with crypto-economic incentives (via tokens tracked by distributed ledgers) and human collaboration (mostly online, relying on both crypto-native and traditional web-based coordination tools). [34] As digital organizations, most DAOs are not tied to a specific location, and have an open door policy when it comes to membership: anyone can join, contribute, and earn a claim to the rights and resources that the DAO distributes. Ideally, a DAO is organized in a way that no individual has full control over its assets and governance while, collectively, the participants can still make decisions and take action to steer its development. Put differently, DAOs aspire to be autonomous in the dual sense of high guarantees of information tracking and transaction execution (autonomous as in automated and resistant to tampering or censorship), and a high degree of organizational self-determination (autonomous as in sovereign, usually involving some form of online voting). [35]

Ideas on the appropriate legal status [36], architecture, and governance of DAOs are evolving rapidly and it is still too early to systematically assess the long-term benefits and shortcomings of particular DAO designs over others. Although DAOs differ in their purpose and activities [37], which naturally results in variation in the challenges faced by individual DAOs, the most pressing universal challenge can be summarized in the following question: how can DAOs perform key organizational functions (e.g. mobilizing and allocating resources, hiring contributors, distributing tasks and decision-making authority [38], resolving conflicts between different stakeholders, ensuring tax and legal compliance, etc.) while staying true to the core principles of crypto? To address this challenge, technical infrastructure and standards tailored specifically to the needs of DAOs are currently being developed. [39] Meanwhile, DAO governance is becoming increasingly professionalized, best practices are beginning to emerge, and the most impactful DAOs are starting to attract the attention of regulators. [40]

It would be sociologically naïve to assume that blockchain networks and DAOs are immune to the typical failure modes of traditional institutions. [41] However, it would be equally short-sighted to ignore the genuine innovation that blockchains combined with advanced ICT infrastructure enable: the ability to coordinate and transact on a global scale by relying on decentralized digital networks instead of centralized legacy institutions. This represents not only a major shift in the context of the ICT Revolution, but more broadly in the evolution of technology towards a planetary system of networked automation.

Crypto as automation

Technological progress tends towards increasingly higher degrees of automation. This tendency has been particularly evident since the Industrial Revolution and has been amplified by the ICT Revolution. The combination of computers, sensors, network communications, and advanced robotics is enabling increasingly sophisticated cyber-physical systems in which a large number of concurrent procedures can be completed at scale with minimal need for human assistance or intervention. While this is most often highlighted in the context of agriculture, manufacturing, transport, and utilities (Industry 4.0), the impact of ICT on automation goes much further.

A core component of digital automation is the administration of the stocks and flows of information, which spans from a handful of files on a personal device all the way to the processing of many petabytes of data per day by global digital platforms. Administering information according to a predefined set of rules (a ’protocol’) is one of the defining features of bureaucracy — a type of organization that defines modernity [42] and is fundamentally aligned with, and empowered by, ICT. The essence of this empowerment is the reduced role of humans in performing an ever-increasing amount of bureaucratic operations: filing cabinets are replaced by digital data storage; manual processing of transactions is replaced by computerized automation; human bureaucrats — the proverbial middlemen — are replaced by distributed (and increasingly global) networks of middlemachines.

Crypto can be thought of as the continuation of administrative digitization and automation triggered by the ICT Revolution. However, by combining automation with decentralization and censorship-resistance, crypto takes a step towards a more ’perfect’ bureaucratic institution, one that (at least on the surface) is more difficult to corrupt and that mindlessly performs — without getting tired of, or forming opinions about — whatever it has been programmed to do. While crypto protocols and networks are still subject to human control, they are also meant to resemble an automaton — an always-available global vending machine that anyone can use, add products to, and service. As different parts of this automaton become integrated with the rest of ICT, the system as a whole can be used as administrative infrastructure for truly global institutions and governance. As a result, crypto will inevitably remain an object of political contention. [43]

Conclusion

The description of crypto presented above, inspired by the neo-Schumpeterian theory of techno-economic paradigm shifts, can be summarized in the following five propositions:

- Crypto is not a technological revolution. It is yet another cluster of innovative activity enabled by ICT (cryptography, computers, software, distributed networks, etc.) and, as such, can only be categorized as part of the ICT Revolution.

- Crypto is partly a reactive, techno-populist reform movement. In terms of its critical stance towards incumbent institutions and the economic power relations inherited from the first half of the ICT Revolution, crypto is typical of the early deployment stage.

- By enabling more ICT-native forms of finance (digital, global, programmable), crypto presents a competitive challenge to incumbent financial institutions, accelerates their digital transformation, and drives financial and regulatory reform tailored specifically for the Information Age.

- Crypto is primarily a process and institutional innovation. By combining the existing capabilities of ICT with innovations in decentralized consensus and coordination mechanisms, crypto enables ICT-native forms of organization that extend beyond just money and finance.

- Crypto represents the continuation of administrative digitization and automation triggered by the ICT Revolution. By enabling more decentralized and censorship-resistant forms of automation, crypto opens up new prospects for global governance and, as such, can be viewed as a central theme in the emerging (geo)political economy of automation.

As the ICT Revolution matures, its most durable legacies are gradually revealed. Whether crypto represents merely a curious sideshow, an important complement to centralized digital platforms, or a more fundamental and far-reaching break with existing institutions, remains to be seen. But regardless of the ultimate role of crypto, the social structure of the future will certainly be more digitally mediated, globally integrated, and automatically reproduced. As a result, the challenge of governing society will increasingly overlap with the challenge of governing a system of digital technology that will outlive its creators and their goals, both empowering and constraining future generations.

Footnotes

[1] Perez, C. (2003). Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. Edward Elgar Publishing. For a more recent discussion by Perez on the periodization of technological revolutions, see Perez, C. (2017–2018). ’Second Machine Age or Fifth Technological Revolution?’ Beyond the Technological Revolution (especially parts 1–3, available here, here, and here).

[2] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 151–157, 165).

[3] A more radical interpretation of the current stage of the ICT Revolution, including the emergence of crypto, is possible by drawing comparisons with the pre-industrial era of Renaissance. See Galbraith, D. (2019). ’New Types of Organization and the Myth of the Return of the City State’. Medium (available here); and Rosenthal, J. (2021). ’The Crypto Renaissance’. Bankless Podcast (available here).

[4] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 14–19, 143).

[5] On Perez’s views on what deployment might entail in the context of the ICT Revolution, see Perez, C. (2018). ’Second Machine Age or Fifth Technological Revolution? (Part 9)’. Beyond the Technological Revolution (available here).

[6] Only in the very long term can societal trends be described in a way that matches the experience of people positioned in radically different geographies or socio-economic strata. Even today, despite historically unprecedented levels of technology adoption, there is still considerable global variation in how people experience not only the ICT Revolution but also earlier forms of technology.

[7] Adapted from Perez, C. (2003). Technological Revolutions and Financial Capital… (especially p. 14); and Perez, C. (2020). ’Technological Revolutions and the Shape of Tomorrow. Why the Future is Not Always the Continuation of the Recent Past’. Presentation at Baillie Gifford (available here).

[8] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 168–171). In 2009 (see [29]), Perez identified the bursting of a ’double bubble’ of technology stocks in the 1990s and early 2000s, and real estate in the 2000s, as the mid-stage of the ICT Revolution.

[9] Andreessen, M. (2011). ’Software is Eating the World’. The Wall Street Journal (available here).

[10] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 23–26).

[11] Many authors have associated financialization with the rise of neoliberalism that started in the 1970s and coincided with the rise of ICT. See Epstein, G. A. (2005). Financialization and the World Economy. Edward Elgar Publishing. For a more recent collection of articles on financialization, see Kornrich, S. & Hicks, A. (2015). Special Issue: The Rise of Finance: Causes and Consequences of Financialization. Socio-Economic Review, Vol. 13, №3.

[12] Universal Basic Income (UBI) and the Job Guarantee (JG) are perhaps the best examples of socio-economic policy ideas that, if implemented at scale during the second half of the ICT Revolution, would be considered as radical as the establishment of the first modern welfare state in Imperial Germany in the 1880s, or the expansion of Western social security systems after the Second World War.

[13] For a critical overview of the social and economic effects of financialization in the United States, including the financialization of non-financial firms, see Donner, L. (2021). ’The Dignity of Work. Testimony Before the Committee on Banking, Housing, and Urban Affairs of the United States Senate’. Americans for Financial Reform (available here). For a similar overview in the context of Europe, see Battiston, S., Guerini, M., Napoletano, M. & Stolbova, V. (2018). ’Financialization in EU and the Effects on Growth, Inequality and Financial Stability’. ISI Growth (available here).

[14] According to Deloitte, the total amount of capital invested globally in fintech companies increased more than 50 times from $1.2 billion in 2008 to $69 billion in 2019, although the number of new fintech firms created peaked in 2014 and the industry has been showing signs of consolidation in more recent years. Meanwhile, according to Pitchbook, the total amount of venture capital invested into crypto companies hit a new all-time record only half way into 2021 at $17 billion, more than double the previous high of $7.4 billion in 2017. See Eckenrode, J. (2020). ’Fintech Investors: Enthusiastic Yet Strategically Picking Their Spots’. Deloitte (available here); and Kochkodin, B. (2021). ’Venture Capital Makes a Record $17 Billion Bet on Crypto World’. Bloomberg (available here).

[15] According to Our World in Data, over 70% of people are using the Internet in most developed economies, with a handful of countries (e.g. Canada, Japan, Norway) showing a 90%+ penetration rate. However, there are still many countries, especially in Africa and Asia, where the vast majority of the population does not have easy Internet access. Adoption is more evenly distributed when it comes to mobile phones. See Roser, M., Ritchie, H. & Ortiz-Ospina, E. (2021). ’Internet’. Our World in Data (available here); and Roser, M. & Ritchie, H. (2021). ’Technology Adoption’. Our World in Data (available here).

[16] For a general introduction to blockchain- and smart contract-based finance (i.e. decentralized finance, or DeFi), see Schär, F. (2021). ’Decentralized Finance: On Blockchain- and Smart Contract-Based Financial Markets’. Federal Reserve Bank of St. Louis (available here). For a list of DeFi protocols and applications, see DeFi Pulse.

[17] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 138–143).

[18] For a general introduction to the topic of financial innovation, see Khraisha, T. & Arthur, K. (2018). ‘Can We Have a General Theory of Financial Innovation Processes? A Conceptual Review’. Financial Innovation, Vol. 4, №4 (available here).

[19] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 128–129).

[20] Perez, C. (2003). Technological Revolutions and Financial Capital… (pp. 131–132).

[21] For an overview of how traditional FOSS governance relates to blockchain networks, see Laul, M. (2020). ’FOSS Governance and Blockchain Networks’. Medium (available here).

[22] In terms of cybersecurity in crypto, it is important to distinguish between the security of data in a blockchain and the security of blockchain-based software applications or centralized service providers (e.g. exchanges) that take full custody of user funds. Security incidents and fraud associated with the latter have little bearing on the security of the former.

[23] Laul, M. (2021). ’Systemic Risk Mitigation in DeFi’. Medium (available here). Systemic risks in DeFi include “risks that could result in large financial losses or other types of damage to many entities simultaneously, leading to the failure of specific institutions, networks, or software protocols in a way that could threaten economic and social stability more broadly. Such risks may stem from a poor understanding of growing complexity, deficiencies in cyber and other security practices, excessive levels of poorly managed financial and counterparty risk (including limited use of insurance and hedging), deterioration of underwriting or other professional standards, lack of transparency, proliferation of fraud, and inadequate rules or oversight, especially around market integrity and consumer protection. […] In comparison to traditional finance, the key technological advantages of DeFi as it relates to systemic risk mitigation are higher levels of digitization, transparency, and automation. [For example, the] more widely DeFi relies on formally verifiable open source code and publicly verifiable ledgers, the easier it will be to set up automated systems of risk simulation, stress testing, monitoring, early warning signals, circuit breakers, insurance cover, claims processing, reporting, and other embedded forms of managing risk [see also [26]]. Ideally, these mechanisms should minimize the likelihood and collateral damage of catastrophic events without radically compromising end user privacy or hindering the growth potential of DeFi, similar to how modern principles of fire safety limit the areas in which fire can freely spread rather than [the overall size of individual buildings or cities].“ Ensuring high levels of end user privacy while keeping large amounts of data publicly verifiable is exactly the type of challenge that cryptography may be able to solve (e.g. by using zero knowledge proofs). However, as of 2021, most of crypto is still far from delivering true end user privacy. See Winter, P., Lorimer, A. H., Snyder, P. & Livshits, B. (2021). ’What’s in Your Wallet? Privacy and Security Issues in Web 3.0’. Cornell University (available here).

[24] Innovation economists distinguish between the ’real’ and the ’symbolic’ element of individual technologies and technological paradigms. The ‘real’ is what exists as the basis for further progress (e.g. prototypes and organizational procedures); the ‘symbolic’ is a set of heuristics around possible directions for new research and development. A similar distinction can be made in the context of communicating the potential of innovation with the broader market. In the early stages of a new product or paradigm, visionary narratives about the future are produced by inventors, entrepreneurs, scientists, journalists, investors, and writers who, by creating a compelling image of what’s to come, attract additional interest and investment. Although these visions are often merely aspirational, their performative effects can easily turn them into self-fulfilling prophecies. The same dynamic is at play in crypto. See Deutschmann, C. (2019). Disembedded Markets: Economic Theology and Global Capitalism (pp. 108–109). Routledge.

[25] For a general introduction to the digitization of money, see Brunnermeier, M. & James, H. (2019). ’The Digitalization of Money’. Princeton University (available here). For a high-level primer on CBDCs, see BIS. (2020). ’Central Bank Digital Currencies: Foundational Principles and Core Features’. Bank of International Settlements (available here). For a discussion of CBDCs in relation to cross-border payment systems, see BIS. (2021). ’Central Bank Digital Currencies for Cross-Border Payments’. Bank of International Settlements (available here). For a discussion of CBDCs in the context of Europe, and the geopolitics of digital money, see IEF. (2021). ’Establishing a Digital Euro: How to Ensure Financial Sovereignty in the Digital Realm’. Internet Economy Foundation (available here).

[26] The idea that ‘code is law’ is closely related to bureaucratic administration (the defining feature of which is operating according to a predefined protocol), software systems as semi-autonomous social structures, and the concept of embedded supervision. See Laul, M. (2019). ’Blockchain Networks Are Bureaucracies Par Excellence’. Medium (available here); Laul, M. (2020). ’On Autonomous Software’. Medium (available here); and Auer, R. (2019). ’Embedded Supervision: How to Build Regulation Into Blockchain Finance’. Bank of International Settlements (available here). Gavin Wood (see here) has recently proposed the term ’autonomation’, defined as “the use of constructed (crypto-)economic incentives to create a digital service or facility able to robustly sustain itself without the explicit intervention or permission of an identifiable human or human-led organisation.“ The same term has previously been used in the context of Toyota’s car manufacturing system where it refers to the idea of “automation with a human touch” — a quality control process in which a machine automatically stops when encountering an abnormal situation, followed by the corrective intervention of a human worker (see here). The appropriate role of regulation and human intervention in crypto is an area of active debate and a key question in the emerging (geo)political economy of automation (see also [43]).

[27] In developed economies, the normalization of more digitally-native lifestyles and work habits was accelerated by the COVID-19 pandemic in which lockdowns forced many individuals and organizations to operate remotely vis-à-vis their workplace and customers. But even though some digital technologies (e.g. smartphones and the Internet) have gained meaningful global adoption, as of 2021, the digital is still far from being the norm for large parts of the global population, especially in the economically less developed regions (see [15]). Here, it is important to remember the geography of technological revolutions and the distinction between core and peripheral countries. It may take significantly longer than 50–60 years for a new techno-economic paradigm to reach the latter at scale and, in some cases, peripheral countries may actually benefit from skipping certain technologies altogether and leaning into the next wave of innovation instead (known as ’leapfrogging’).

[28] Governance can be defined as the process of applying any design feature or control mechanism — regardless of whether implemented by humans or machines — that maintains and steers a system. On crypto governance, see Laul, M. (2020). ’Ten Theses on Decentralized Network Governance’. Medium (available here); and Schneider, N. (2021). ’Cryptoeconomics as a Constraint on Governance’. OSF (available here). Schneider is critical of economic incentives and financialization as governance mechanisms (which he associates with neoliberalism), and highlights the role of democratic politics as a necessary counterweight (see also [30]). For a commentary on Schneider’s article by Vitalik Buterin, one of the most prominent voices in crypto, see Buterin, V. (2021). ’On Nathan Schneider On the Limits of Cryptoeconomics’. Vitalik Buterin’s Personal Blog (available here).

[29] Each technological revolution has many unique characteristics, which means that developing a model that applies to all historical cases is feasible only at a very high level of generalization. In the early 2000s, when Perez published [1], an empirical account of the second half of the ICT Revolution was out of the question, and it was possible to merely anticipate the nature of the deployment stage based on historical comparisons. In 2009, Perez drew a distinction between major technology bubbles (MTBs) that result from an ’opportunity pull’, and easy liquidity bubbles (ELBs) that result from a credit push. According to Perez, the mid-stage of the ICT Revolution was indicated by the bursting of two financial bubbles. The technology stock boom of the 1990s was an MTB, but the eventual crash was too contained to trigger a policy response that favored the real economy over finance. The credit boom of the 2000s was an ELB, and the 2007–08 crisis was deep enough to spark general dissatisfaction with the financial sector, opening the door for deployment stage institutional reform. See Perez, C. (2009). ’The Double Bubble at the Turn of the Century: Technological Roots and Structural Implications’. Cambridge Journal of Economics, Vol. 33, №4, pp. 779–80 (working paper version available here). Between 2001 and 2021, the digital economy went through a major restructuring, which is something that Perez does not yet recognize in her 2009 article. Digital technology companies (production capital) emerged as some of the most powerful organizations in the world, albeit not at the expense of the financial sector, which is one important feature that distinguishes the Information Age from previous technological revolutions. Meanwhile, the social and institutional transformations triggered by the ICT Revolution are highly dispersed and it is still too early to assess which of these transformations, in retrospect, will be considered most impactful. The use of the term ’deployment stage’ in this context should therefore be understood in a dual sense: first, as it’s used in Perez’s descriptions of previous technological revolutions, where its meaning is more narrowly fixed; and second, as signifying the impact of ICT on society over the past couple of decades (and beyond), where its meaning is still open and evolving.

[30] Full democratic control over base layer public blockchain networks via government institutions is oxymoronic because one of the core value propositions of blockchains is decentralization, which includes independence from centralized governance. However, blockchain networks are not entirely immune to democratic checks and balances. For example, governments could introduce laws or regulations that directly affect the ease of operating and using blockchain networks, and software developers, network administrators, and consumers have the option to ’democratically’ coordinate in ways that either strengthen or weaken a particular network. In practice, most blockchain networks and DAOs tend to be informally technocratic by default, which means that most critical functions are performed by technical experts. Even though there are strong ideological objections to more formal and inclusive governance mechanisms (which are seen as opening the door to explicit political bickering and capture), many network communities and DAOs have implemented formal voting systems (e.g. to signal support for software upgrades or allocating common pools of resources) in which votes are weighted according to the amount of coins or tokens that each voter controls. The resulting system resembles a plutocracy. As of now, more democratic forms of network and DAO governance are underexplored and raise some difficult questions. Who or what defines the demos, the constituency? Are there sufficiently secure and privacy-preserving voting solutions available? Which decisions should be controlled by a popular vote? Should it be possible to delegate votes? If so, how should the rights and responsibilities of delegates be defined (see also [38])? For decentralization purists and proponents of minimal formal decision-making involving humans, these questions are anathema, and are likely never to be legitimately raised in the context of some blockchain networks. But that does mean that, in the long term, democratic checks and balances won’t play an important role in any network whatsoever.

[31] Over the course of the ICT Revolution, digital governance, i.e. “the use of digital tools to guide and manage personal lives, organizations, markets, and societies… [and] the control and management of information technology systems,“ has started to increasingly overlap with societal governance more broadly. For a high-level taxonomy of digital governance, see Laul, M. (2021). ’The Evolving Landscape of Digital Governance’. Medium (available here).

[32] There is some overlap between blockchain networks and DAOs, but the two terms are not synonymous. Communities that develop and operate blockchain networks may or may not self-identify as DAOs and, more often than not, individual DAOs (see [37] for examples) rely on the services provided by blockchain networks that the DAO has no direct control over. In more traditional settings, this would result in considerable platform risk. However, in the case of sufficiently decentralized blockchain networks, platform risk is reduced due to high levels of tamper- and censorship-resistance. See also Burniske, C. (2018). ’Cryptonetworks are not Companies’. Medium (available here); and Grossman, N. (2019). ’What Decentralization is Good For (Part 2): Platform Risk’. Nick Grossman’s Personal Blog (available here).

[33] Smart contracts are computer programs that execute automatically under certain predefined conditions. In the context of crypto, these computer programs are stored and processed by blockchain networks.

[34] In some cases, especially in the field of blockchain-based application development, coordination may be distributed only in a very limited sense (e.g. through relying on external decentralized infrastructure, and by sourcing contributions from a geographically distributed workforce or community) with many critical governance mechanisms concentrated in the hands of a small group of core contributors. To reduce such concentration of power, many teams have formalized plans to ’progressively decentralize’ — a concept popularized by Jesse Walden. See Walden, J. (2020). ’Progressive Decentralization: A Playbook for Building Crypto Applications’. Andreessen Horowitz (available here). But regardless of where a particular network or DAO falls on the decentralization spectrum, it is undeniable that crypto opens up new possibilities for living, working, and organizing online. For a discussion of crypto and digitally-native work arrangements (self-directed, remote, ad hoc, pseudonymous), see Hoffman, D. (2021). ’The Future of Work’. Bankless (available here). For a discussion of how the structure and governance of DAOs relate to earlier forms of online community, such as gaming guilds, see Kreutler, K. (2021). ’A Prehistory of DAOs’. Mirror (available here).

[35] The distinction between autonomy as automation and autonomy as sovereignty is borrowed from James Duncan. See Duncan, J. (2021) ’D(?)A(?)O — Decentralization and Autonomy in “DAOs”’. Mirror (available here). See also, Monegro, J. (2019). ’Sovereign Cryptonetworks’. Placeholder (available here). A third meaning of autonomy in the context of DAOs relates to the autonomy of individuals, describing DAOs as ‘leaderful’ as opposed to leaderless organizations. As DAOs develop more formal structure and professionalize (see [40]), the autonomy of the individual relative to organizational prescriptions and hierarchy is likely to decrease. For a connection between autonomy and the idea that ‘code is law’, see [26].

[36] As is often the case with rapid innovation, DAOs currently exist in a legal grey zone. Three perspectives on the legal status of DAOs can be distinguished. The first one presents DAOs as pure cyberspace organizations that are able to crowdsource contributions and deliver services over the Internet without having to rely on traditional legal and financial systems. According to this view, any attempt at creating a regulatory framework for DAOs undermines their core purpose of bypassing traditional rules and institutions. The second approach recommends categorizing DAOs as unincorporated associations or (digital) cooperatives, making it possible to use existing legal categories as a starting point for regulating DAOs. The third view accepts that DAOs are a fundamentally new form of organization, but recommends creating a separate category within existing legal frameworks, thus opening the door for regulating DAOs through traditional institutions but possibly in an unprecedented way. The most prominent early example inspired by the third approach is the Wyoming DAO bill (available here). For a discussion of DAOs as cooperatives, see Walden, J. (2019). ’Past, Present, Future: From Co-ops to Cryptonetworks’. Andreessen Horowitz (available here); and Walden, J. & Spelliscy, C. (2020). ’Leadership in The Ownership Economy — Scaling Decision Making while Minimizing Securities Risk’. Variant Fund (available here). For a general overview of the advantages of DAOs over traditional forms of organization, and the associated legal challenges, see Wright, A. (2021). ’The Rise of Decentralized Autonomous Organizations: Opportunities and Challenges’. Stanford Journal of Blockchain Law & Policy (available here). For a list of the most pressing questions for DAOs based on interviews with DAO stakeholders, see Spelliscy, C. (2021). ’Scaling DAOs Won’t Be Easy: Five Major Challenges to Overcome’. The Defiant (available here). In September 2021, the venture capital firm Andreessen Horowitz published a detailed proposal to the United States Senate Banking Committee on how to regulate crypto, including DAOs (see here).

[37] For examples of different types of DAOs, see Turley, C. (2021). ’DAO Landscape’. Mirror (available here); and DeepDAO dashboard.

[38] An important recent development in DAO governance is the growing popularity of vote delegation, whereby token holders who don’t have the desire or resources to participate in the day-to-day governance of a DAO (which usually involves tracking and voting on governance proposals) can delegate their voting power to other individuals, groups, or organizations. See Amico, J. (2021). ’Open Sourcing Our Token Delegate Program’. Andreessen Horowitz (available here).

[39] In addition to the underlying blockchain networks and open source protocols, infrastructure and tooling is being created for the following functions: launching DAOs; tokenizing assets and claims; accounting; managing identities, reputation, and tasks; collaborating on software code; administering the proposal lifecycle and voting procedures; operating treasuries and other common pools of resources; and curating DAO-related information. See Kesonpat, N. (2021). ’Organization Legos: The State of DAO Tooling’. Medium (available here). Many DAOs also rely heavily on conventional web-based coordination tools such as Github, Discourse, Discord, Notion, Twitter, and Telegram, as well as external, centralized service providers, especially as it relates to accounting, payroll, taxes, and insurance (e.g. Opolis).

[40] Professionalization, imitation, technical standards, and regulatory pressure are all drivers of institutional isomorphism, i.e. growing similarities between independent organizations operating in the same field. See Laul, M. (2021) ’Isomorphism in DAO Governance’. Medium (available here).

[41] The social and economic track record of crypto is currently not long enough to assess the shortcomings and possible failure modes associated with different rulesets or governance structures, and whether crypto represents a merely technical, or a much deeper, improvement over legacy institutions. See Atzori, M. (2017). ’Blockchain Technology and Decentralized Governance: Is the State Still Necessary?’ Journal of Governance and Regulation, Vol. 6, №1, pp. 45–62 (available here); Laul, M. (2018). ’Resource Distribution and Power Dynamics in Decentralized Networks’. Medium (available here); and Laul, M. (2019). ’The Full Circle Hypothesis’. Medium (available here). See also [28].

[42] Max Weber famously identified the rise of bureaucratic organization as part of the overall rationalization of modern society. The adoption of ICT and crypto can be viewed as the evolution of bureaucracy towards a more digital, global, resilient, and automated form. However, it would not be entirely accurate to identify it as part of the continued “disenchantment of the world“ because — to use Arthur C. Clarke’s well-known phrase — “any sufficiently advanced technology is indistinguishable from magic.“ Even though Weber’s nationally defined ’iron cages’ of bureaucracy are being replaced by a global ’silicon cage’, digital progress simultaneously produces a world that, even by the standards of as recent a time as the early 20th century, is technologically magical. See Laul, M. (2019). ’Blockchain Networks Are Bureaucracies Par Excellence’. Medium (available here); Weber, M. (1922). ’Bureaucracy’. From Gerth, H. H. and Mills, C. W. (eds.), Max Weber: Essays in Sociology (pp. 196‐266). Oxford University Press (available here); and Weber, M. (1946). ’Politics as a Vocation’. From Gerth, H. H. and Mills, C. W. (eds.), From Max Weber: Essays in Sociology (pp. 77‐128). Oxford University Press (available here).

[43] By enabling ICT-native institutions and forms of governance, crypto represents a central theme in the emerging political economy of automation, which includes the question of whether blockchain governance is compatible with concepts such as democratic checks and balances and public accountability. See Laul, M. (2021). ’The Great Automaton’. Medium (available here).

The author’s work is funded by Placeholder, a venture capital firm that invests in open blockchain networks and Web3 services.

This article has been cross-published on Crypto, Culture, & Society.

Related Writings

Middlemachines (January 2022)

Isomorphism in DAO Governance (May 2021)

The Evolving Landscape of Digital Governance (February 2021)

The Great Automaton (December 2020)

On Autonomous Software (March 2020)

Blockchain Networks Are Bureaucracies Par Excellence (May 2019)